Mobile Wallets are Where FIs Will Win Their Customer’s Next Transaction

Mobile wallets are a core interface for customers to interact with their financial institutions. With dynamic wallet passes, banks and fintechs can deliver real-time engagement and drive measurable revenue at every stage of the customer journey.

Mobile wallets have transformed how customers interact with their banks. Over 120 million Americans now carry their financial credentials in Apple and Google Wallet instead of a physical card. For financial institutions and fintechs, this is a fundamental shift in how customers manage their money.

The institutions winning today aren't treating mobile wallets as an afterthought. They're redesigning their entire engagement strategy around the mobile wallet platform.

How Wallets Are Evolving Beyond Simple Payment Tools

Wallets used to be simple. Add a card, tap at checkout, done. Now they carry the full customer relationship.

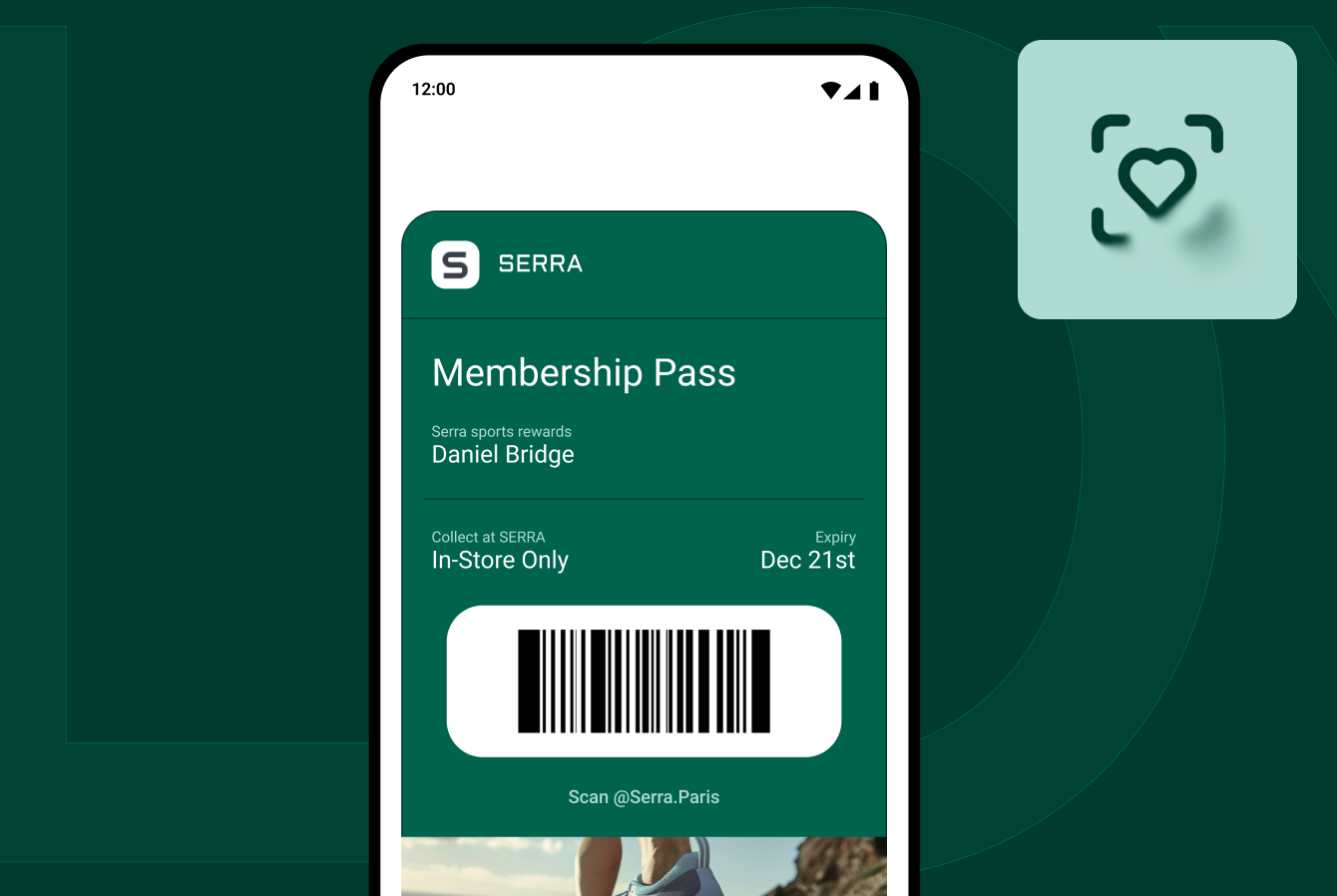

Customers add loyalty cards, membership IDs, and gift cards as wallet passes and use them in stores and online. The wallet is a persistent interface where customers increasingly expect to interact with their financial institution. Every interaction is measurable. Every action connects directly to customer behavior and business outcomes.

Most FIs have a payment card in the wallet, but that card does one thing: tap-to-pay. It can't send a message, update a balance, or surface an offer. A Badge-powered wallet pass changes that. The pass sits alongside the card as a dynamic, programmable companion. The card handles the transaction. The pass handles everything around it.

Which Customer Demographics Are Driving Mobile Wallet Adoption

Who's adopting wallet technology fastest? High earners and younger generations are more likely to adopt and actively use Apple and Google Wallets. According to PYMNTS research, the data shows a clear picture:

— High earners: 61% of people earning $150,000+ report higher spending when using mobile wallets

— Gen Z: Leads adoption across all age groups

— Millennials and Gen X: Catching up rapidly with high transaction volumes

— Baby boomers: Increasingly relying on wallets

These are your best customers. The ones with the highest lifetime value, the most transactions, and the ones driving brand relationships. The mobile wallet is where your customers already are. The question is whether you'll meet them there.

How Financial Institutions Can Build Complete Financial Identity in Wallets

Customers already trust Apple and Google Wallet with their most sensitive credentials. Cards, IDs, and account access live there by default. For financial institutions and fintechs, that trust is the starting point for building a persistent customer connection.

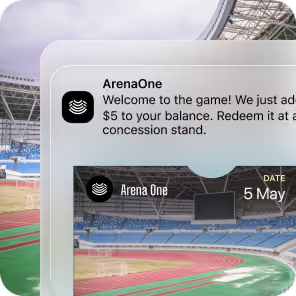

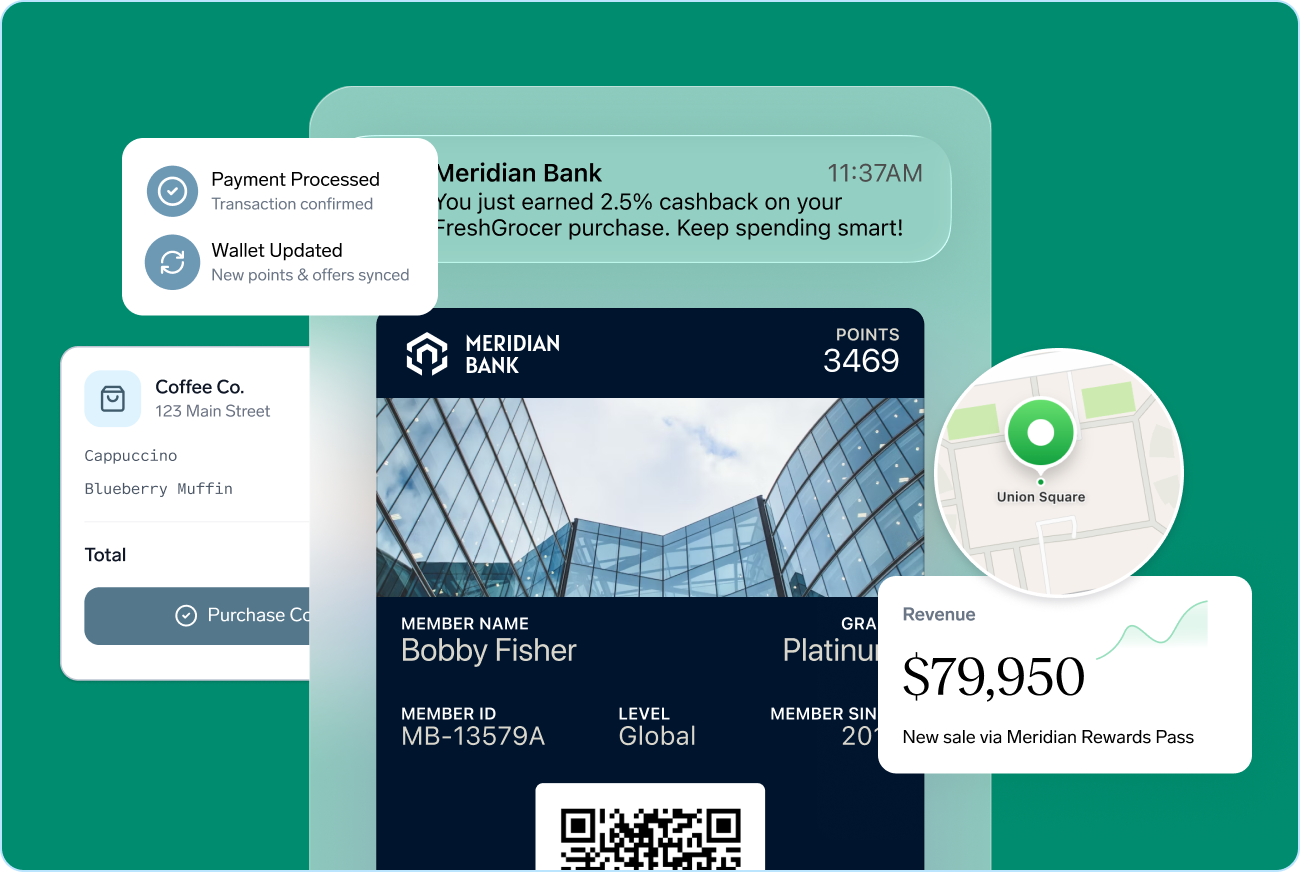

A dynamic wallet pass issued through Badge carries live account data, rewards balances, status tiers, and offers. It updates automatically when a transaction posts, when a reward is earned, or when a credit offer becomes available. Customers receive real-time notifications to the lock screen at moments that matter most.

Wallet infrastructure enables FIs and fintechs to:

— Drive primacy in the wallet: Secure wallet real estate beyond tap-to-pay by delivering a dynamic, programmable surface. Customers engage with your brand at every wallet open, not just at payment.

— Keep customers engaged between transactions: Real-time balance and rewards updates give customers a reason to open the wallet without requiring a branch visit or app session.

— Deliver incremental revenue: Wallet passes are dynamic and always present. You can influence behavior at moments that matter, surfacing offers and upgrades when customers are most likely to act.

— Reach customers at the right moment: Geo-fenced triggers reach customers near a branch, an ATM, or a partner merchant with exactly the right message at exactly the right time.

Measuring Mobile Wallet Engagement From First Add to Revenue Impact

When customers add a wallet pass, they're automatically opted into notifications. This creates a real-time connection to deliver relevant content at the right moment. Geo-triggered messages reach customers near a branch, and real-time balance and rewards updates keep customers engaged between transactions.

Every interaction is measurable, from the moment a customer adds the pass through to revenue impact. FIs can see:

— How many customers added the pass

— How often they open the wallet

— Which notifications drove action

— How many redeemed offers or earned points

— Revenue influenced at each step

This data feeds back into the next campaign. Personalization becomes precise because it's based on actual customer behavior, not guesses or demographics.

Why Badge is Purpose-Built for Wallet Infrastructure at Scale

Badge makes wallet passes programmable at scale. Passes are issued, updated, and measured with full attribution from first add through to revenue impact. Badge integrates with your existing systems, from core banking platforms to loyalty systems to marketing infrastructure.

Passes are issued at scale and updated programmatically. Marketers can launch campaigns in days without engineering bottlenecks. Developers get full API control for real-time updates and customization. The institutions moving on this aren't running one-off campaigns. They're building wallet infrastructure into their core customer experience stack, establishing an authenticated connection to their best customers before the wallet gets crowded.

Why the Window for Wallet Adoption Won't Stay Open

Wallets come pre-installed on nearly every smartphone. Over 120 million Americans use Apple and Google Wallet. By 2030, wallet transaction volumes are projected to exceed $28 trillion. Customers already expect to find financial credentials in their wallet.

The infrastructure is ready. The behavior is established. The customers are already there. What's missing is adoption from FIs. Most institutions haven't moved. Most customers haven't experienced wallet-based engagement from their bank. This creates an immediate window for institutions willing to act.

That window won't stay open forever. Once the wallet gets crowded, once every major FI has a pass, the differentiation fades. Today, being in the wallet is a differentiator. Tomorrow, it will be table stakes.

Will you establish that relationship now, or will you be playing catch-up later?

Apple and Google Wallet are already on your customers' phones. Your brand needs to be there to meet them.

Get in touch at FI@trybadge.com or explore Badge for financial services.